Staggering defence industry backlogs in Europe

If you’re a casual observer of the defence sector, you might have missed the size and scope of the backlogs.

If you’re a casual observer of the defence sector, you might have missed the size and scope of the backlogs.

A backlog is the total value of confirmed orders a company has received but has not yet delivered or recognized as revenue.

Europe’s top 10 defence firms have seen exponential increases in order backlogs over the past year.

Sorted by Defense News Top 100 2025 list - here’s the top 10 European defence firms & order backlogs:

BAE Systems (UK): £83.6B

Thales (France): €16.8B

Leonardo (Italy): €47.3B

Airbus (Netherlands/France): €46.8B

Rheinmetall AG (Germany): €55B

Rolls-Royce (UK): £18.8B

Saab AB (Sweden): SEK 275B

MBDA (France): €37B

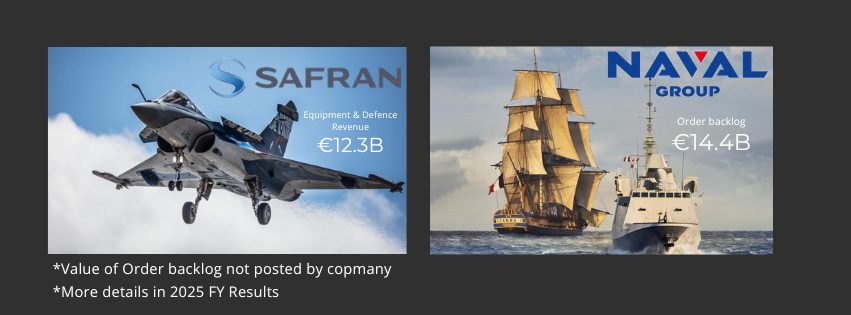

Safran (France): does not provide backlog data

Naval Group (France): €14.4B

TKMS (Germany): €18.7B (not on the DN list but included given current Canadian interests)

The backlogs signal continuous demand growth in the defence sector.

What’s driving the backlog surge?

Multi-year procurement cycles replacing ad-hoc replenishment

Industrial policy shifts (Buy European momentum)

Ammunition & air defence restocking

Capacity expansion financing at the EU level

The key point: backlog growth is a signal that Europe is moving from peace dividend industrial logic to persistent readiness.

Why this matters for Canada

For Canadian firms, the opportunity is huge:

• European primes are supply-chain hungry

• Industrial capacity (not price) is becoming the constraint

If Europe sustains 2%+ spending across major economies, backlog compression will take years, reshaping transatlantic defence trade. Primes and tiers are actively looking for secondary, tertiary, and alternative sources of supply.

P.S. Feel free to reach out with any corrections on year-end figures - year-end season made this a moving target!

Thank you for the article. What are the chances of establishing licensed production of some of these industries in Canada?